As the UK switches from an industrial base to a technological base, the real economy is being downsized.

Large-scale physical investments are higher risk and demand more confidence in the future viability of the nation as a good location to manufacture. Britain increasingly does not meet this benchmark.

We see Britain’s decline in the loss of sovereign capabilities like steel-making or the manufacture of ferro-titanium. We see it in the closing of refineries and chemical facilities. We see it in the decline of military shipbuilding capacity, or other defence-related debacles like Ajax.

The reasons for this are manifold: onerous regulations, lack of protectionism versus unfair trade practices, the struggle to build anything, and, of course, sky-high energy prices.

This last issue is ironic, because there has been an enormous investment in energy infrastructure – more specifically, “renewable” energy infrastructure, which is not productive and may consume more than it produces

In short, after years of rolling out expensive renewable infrastructure, the British energy grid is “more wires for less power,” and possibly will have cost more in energy to set up than it will ever produce.

Let’s not lose touch…Your Government and Big Tech are actively trying to censor the information reported by The Exposé to serve their own needs. Subscribe to our emails now to make sure you receive the latest uncensored news in your inbox…

The following are two separate sources which complement each other.

The first is an interview with Dr. Lars Schemikau, who argues that “green energy,” in some cases, consumes more energy than it produces.

The second is an article by Rian Chad Whitton, who demonstrates that although there has been enormous investment in expensive “renewable” energy infrastructure, less has been produced.

Approaching the topic from different aspects, both sources highlight how expensive and unproductive “renewable” or “green” energy is.

𝐖𝐡𝐚𝐭 𝐈𝐟 “𝐆𝐫𝐞𝐞𝐧 𝐄𝐧𝐞𝐫𝐠𝐲” 𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐬 𝐌𝐨𝐫𝐞 𝐄𝐧𝐞𝐫𝐠𝐲 𝐓𝐡𝐚𝐧 𝐈𝐭 𝐏𝐫𝐨𝐝𝐮𝐜𝐞𝐬?

In a recent interview with Freedom Research, energy expert Dr. Lars Schernikau argues that the hidden energy and raw material costs of large-scale wind and solar are so enormous that some systems may struggle to ever pay back the energy invested to build them.

If you are unable to watch the video above on Rumble, you can watch it on YouTube HERE or on Substack HERE. There is also a commentary about the interview written by Freedom Research below the video on Rumble and Substack.

Taking Stock: The explosion of the energy capital stock in Britain

Table of Contents

Taking Stock of the British Economy

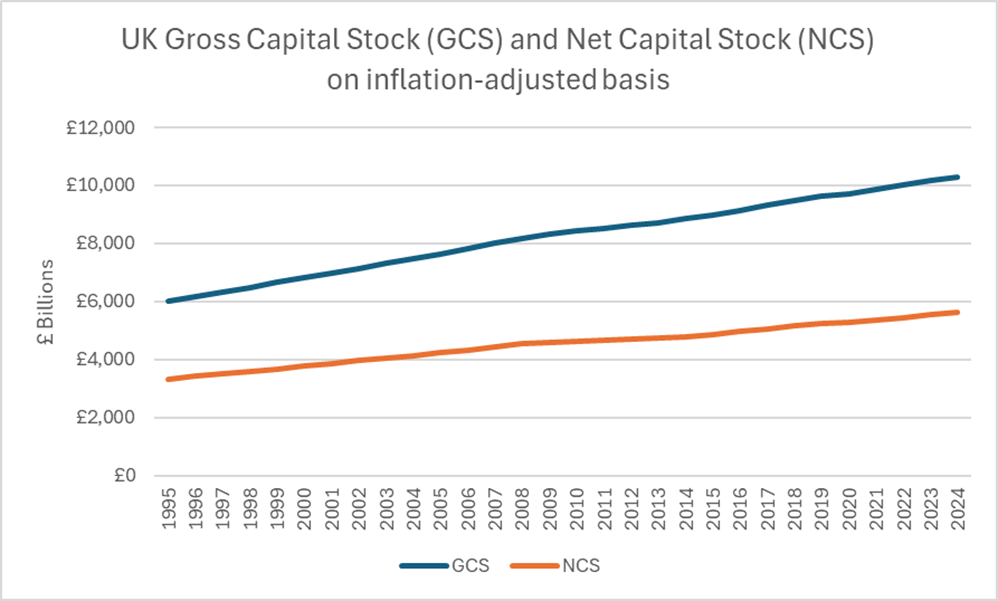

There are many ways to measure the growth of different sectors of the country. GVA, production indexes, employment and investment are all key indicators. One important metric is the gross and net capital stock. Gross capital stock is the total value of all capital assets at their original cost. Net capital stock is the same, but after subtracting depreciation.

For the whole British economy, the gross capital stock has grown in real terms from £6 trillion in 1995 to £10.3 trillion in 2024. The net capital stock grew from £3.4 trillion to £5.6 trillion.

The capital quality ratio (gross – net) has therefore declined from 57% to 54%. While investment has grown, slightly more of it is worn out and old. This chimes with our understanding of British investment, where, compared with other countries, gross capital formation has been relatively low.

We can see a clear correlation between capital stock per worker and productivity. British capital stock per worker is relatively low, and so British workers have far less capital available to be productive than their European or American peers.

There are two key things to consider when analysing capital stock: the shifts in investments across different sectors, and where investment goes in those sectors. This piece will focus specifically on manufacturing and the electricity and gas sector since 1995. There has been a remarkable shift in the relative size of both industries.

Island of No Machines: The Stock of Machinery Has Declined

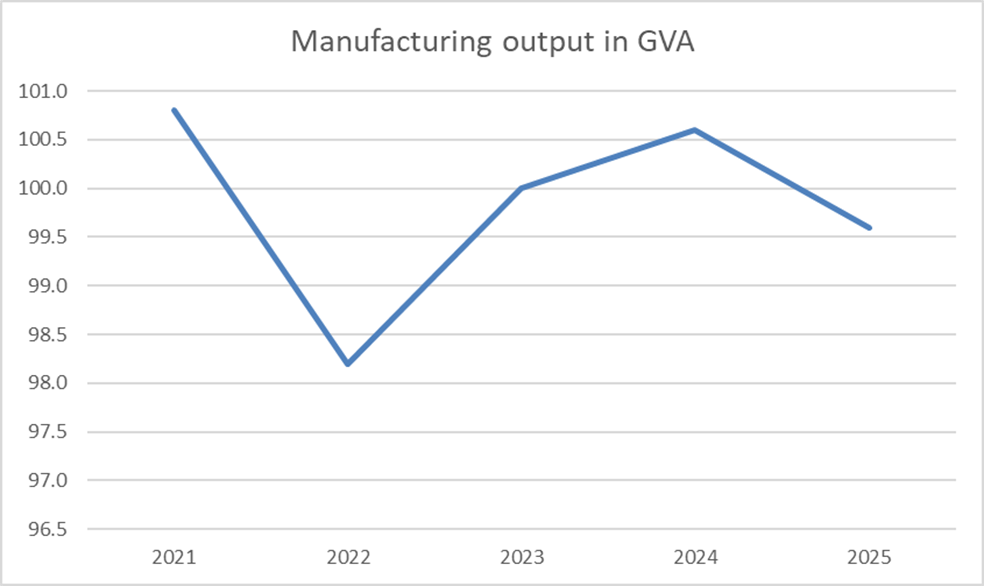

It is well known that British manufacturing has not been growing for some time. Many of the industries have not hit the output they reached in 2008 when adjusting for inflation. From 2021 to 2025, overall output declined.

There are bright spots. Manufacturing has become more high-value added. Output was flat, but the workforce dropped from 4.2 million to 2.5 million. Most of this drop occurred before 2008, however. Since 2008, manufacturing in general has been largely stagnant.

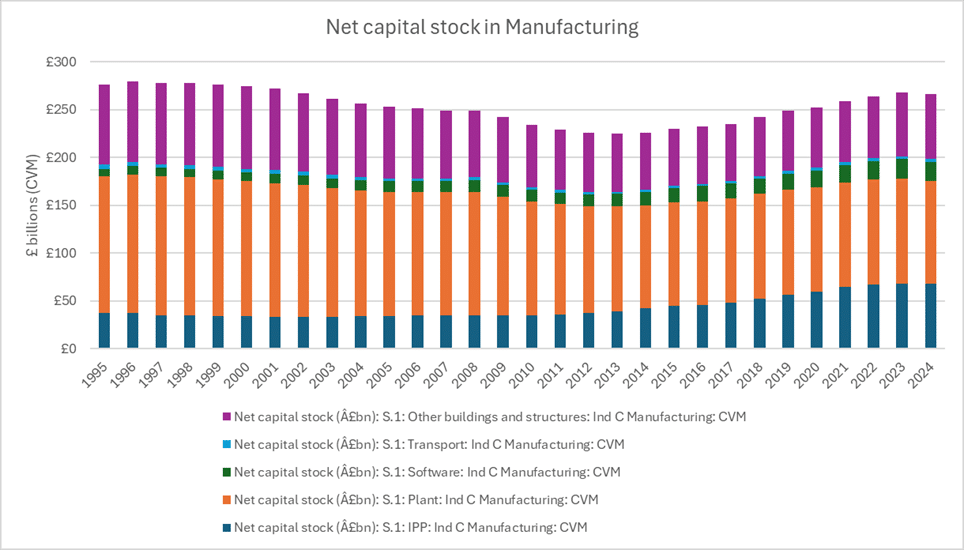

What is particularly interesting in manufacturing is the change in where money is being invested. The Office for National Statistics (“ONS”) splits capital stock into a few categories.

- Intellectual Property Products (“IPP”): Intangible assets representing knowledge and innovation, including research and development (“R&D”).

- Software: In-house developed software as well as data assets.

- Plant equipment and machinery:Physical equipment used in manufacturing and industrial production, such as machine tools, robots, pumps, drives, forge presses and cranes.

- Transport equipment: Assets used to move people and goods, including wheeled vehicles, aircraft, ships, and trains.

- Other buildings and structures: Non-residential buildings and infrastructure such as offices, factories, warehouses, roads and utilities.

The structural importance of these relative investments has changed substantially over time. In 1995, plant equipment and “other buildings and structures,” meaning the factories themselves, were the dominant component of industrial investment, accounting for 82% of all the net capital stock.

Of course, we would expect that as software and intellectual property became more important in the early 21st century, this would change. Up to 2008, buildings and machinery still made 80% of the capital stock in manufacturing, but since then, their relative importance has decreased, reaching just 66% of the capital stock in 2024.

Meanwhile, intellectual property products and software grew from 16% in 2008 to 33% in 2024. As seen below, the net capital stock overall declined from 1995 to 2012, and then made a tepid recovery, boosted by intellectual property, R&D investment and software spending. Although there has been an aggregate increase in the total capital stock since 2008, it has still not reached its 2002 level.

So, fewer machine tools, forges and factories, balanced by more research and development, software spending and intellectual property. We can say that British manufacturing revenue is now more tied to software, design, intellectual property royalties and engineering services than it was. Industry became smarter, more centred around laboratories and research facilities, and more focused on design and office work. Unfortunately, this didn’t lead to any notable increase in output or industrial capacity, and it certainly hasn’t given us more market share.

Of course, all manufacturing is becoming more knowledge-intensive. But the gap does highlight some problems. Software and research spending is relatively low-risk and can be funded by retained earnings. If problems occur, the investments can be unwound much more easily. Large-scale physical investments are higher risk and demand more confidence in the future viability of the nation as a good location to manufacture. Britain increasingly does not meet this benchmark. Regulations make building things hard. The hollowing out of the supply chain makes lead times for critical components far less easy to predict, and there is very little expectation that a British company could take a sizeable chunk of an expanding industrial market like drones, batteries or satellites.

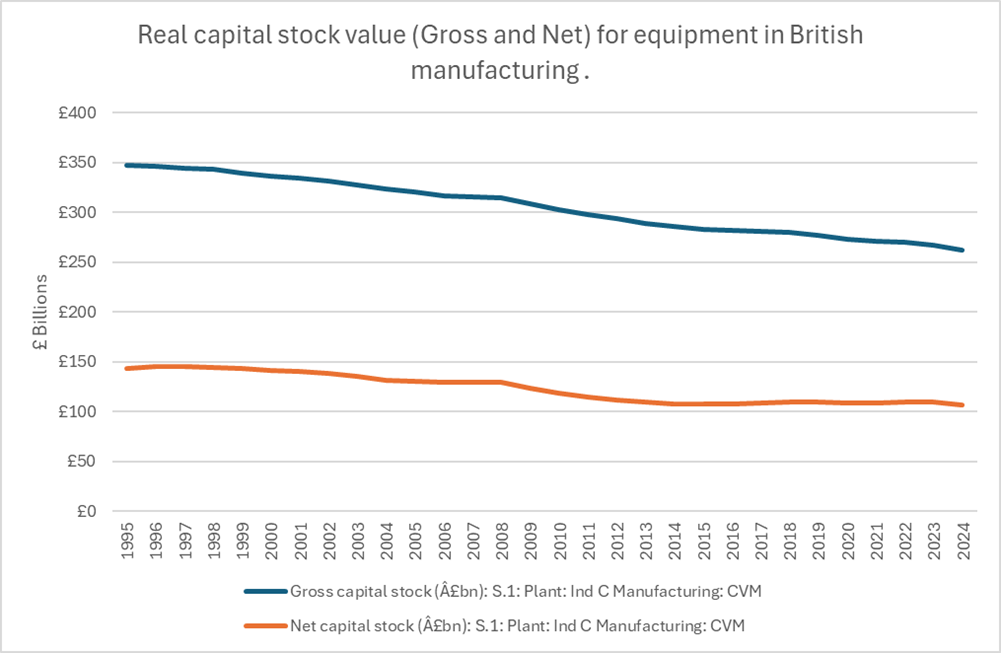

The alarming thing is not that equipment and building investment became relatively less important; it is that it declined so markedly. Let us be generous and ignore the drop in investment from 1995 to 2008, when manufacturing was being moved offshore to East Asia at a particularly fast rate. From 2009 to 2024, the real net capital stock for plant machinery and equipment dropped from £124 billion to £107 billion. For buildings, it dropped from £54 billion to £51 billion.

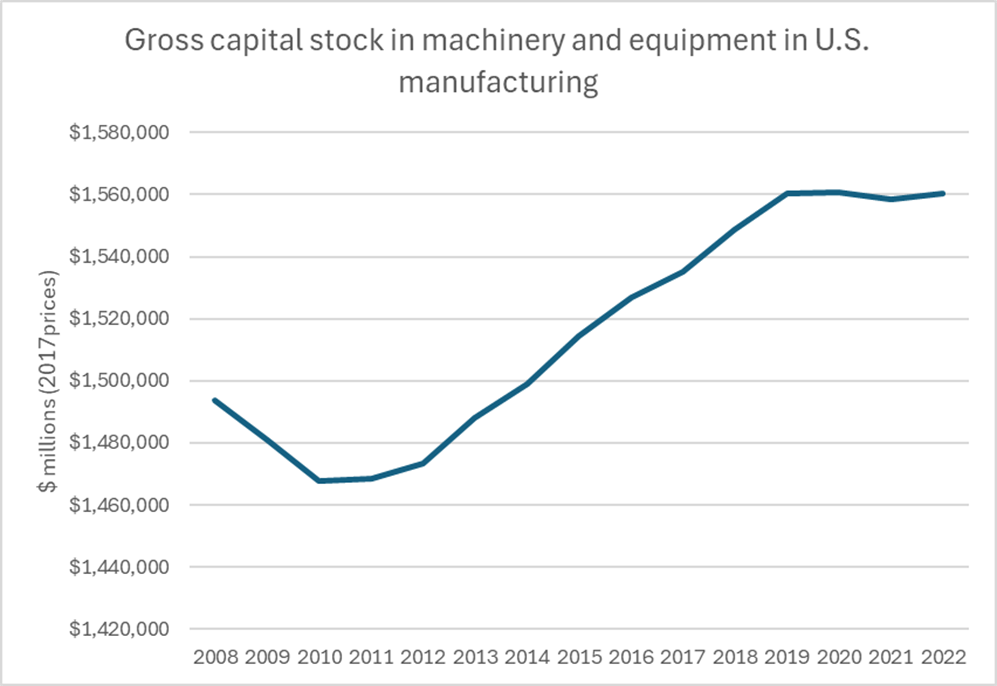

Britain compares quite poorly internationally on this. The US is similar to Britain insofar as manufacturing has played a continuously smaller role in GDP, the economy is highly financialised and has been a major net-importer of manufactured goods for decades. From 2009 to 2022, the real value of the US capital stock in manufacturing equipment grew by $80 billion.

Though far from meteoric, the story is demonstrably better than that of Britain. Since 1995, roughly a third of the value of machinery and equipment in British factories has evaporated.

We see this in Britain’s dearth of robots and machine tools. We see it in the loss of sovereign capabilities like steel-making or the manufacture of ferro-titanium. We see it in the closing of refineries and chemical facilities. We see it in the decline of military shipbuilding capacity, or other defence-related debacles like Ajax.

The reasons for this are manifold. onerous regulations, lack of protectionism versus unfair trade practices, the struggle to build anything, and, of course, sky-high energy prices. This last issue is ironic, because there has been an enormous investment in energy infrastructure.

The Capital Stock Bonanza in Electricity and Gas

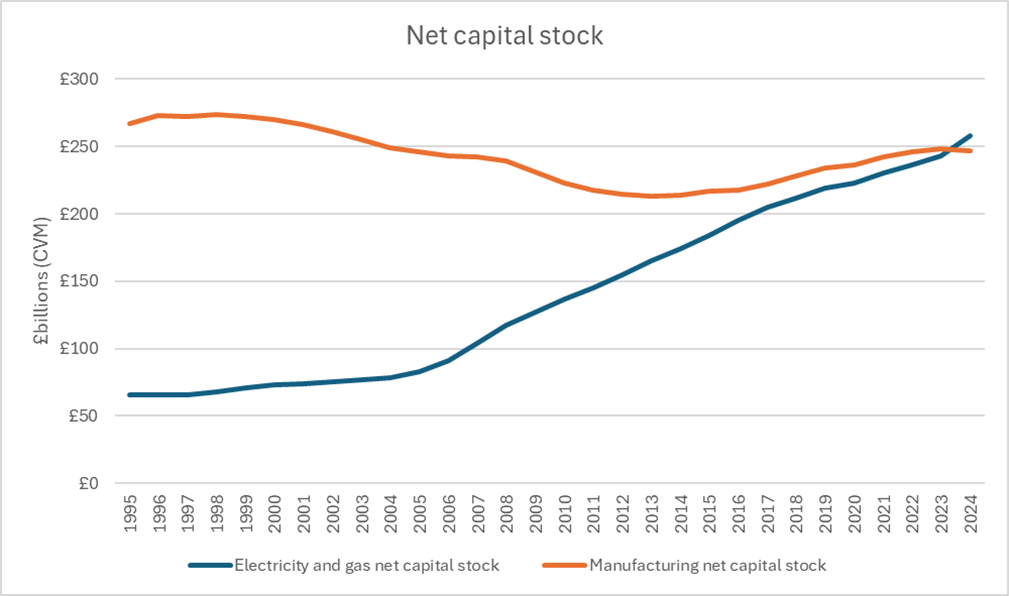

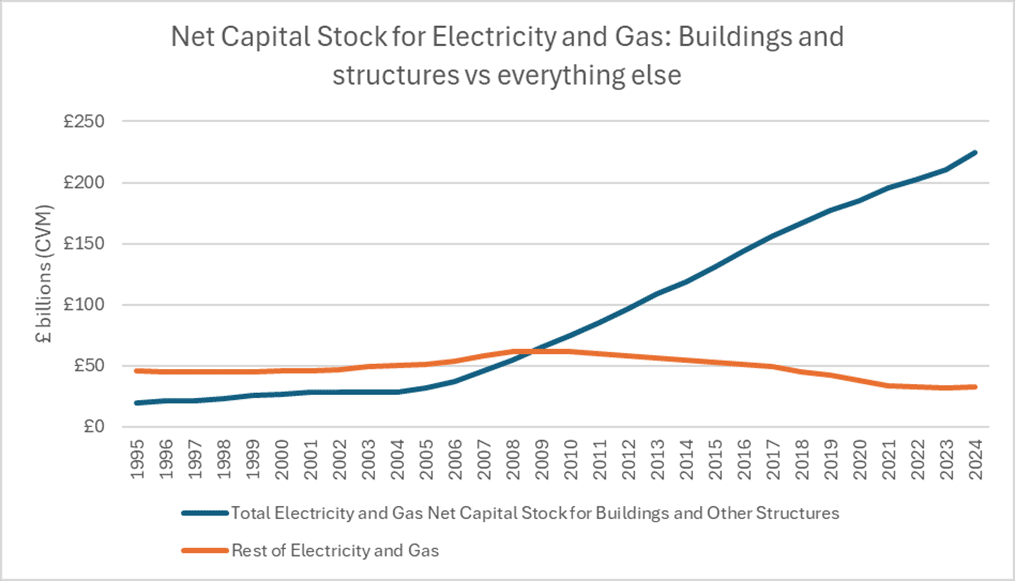

One would intuitively think that having very high energy costs, which we all by now know Britain has, was the result of neglect from businesses and politicians. In fact, during the 21st century, the capital stock of the electricity and gas sector, effectively the entire non-transport energy sector in Britain, has exploded. From 1995 to 2024, the gross capital stock of electricity and gas went from 22% of the value of manufacturing to 71%. The net capital stock of electricity and gas, when accounting for depreciation, went from £66 billion to £258 billion, more than the net capital stock of manufacturing.

When looking at the growth in detail, the vast majority is listed as “other structures,” meaning wind turbines, solar arrays and the transmission and distribution infrastructure necessary to accommodate them. Machinery and equipment, meaning gas turbines, steam turbines, pumps and cooling systems, have not grown at all. This is therefore a clear illustration of the gigantic renewables buildout since 2004.

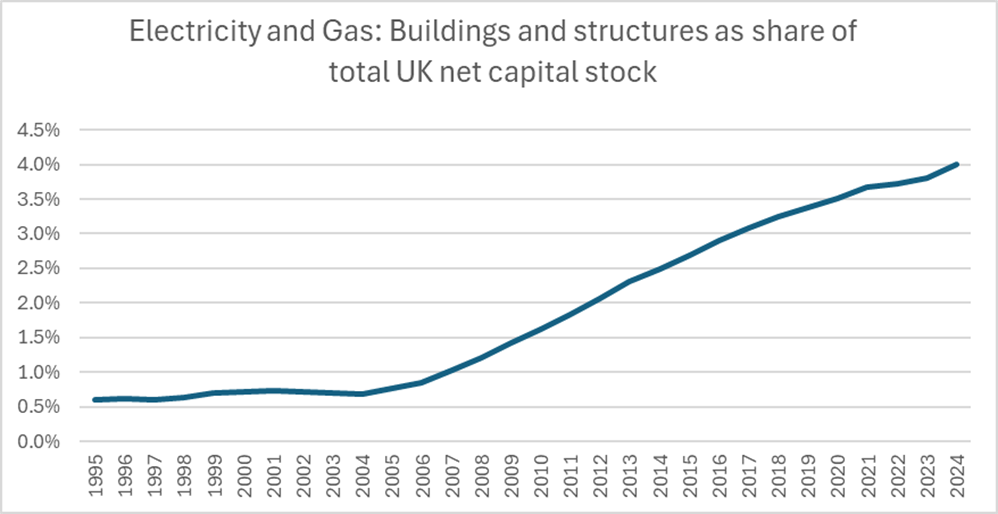

Astonishingly, buildings and structures relating to electricity and gas went from 0.6% of the UK’s total net capital stock in 1995 to 4% today.

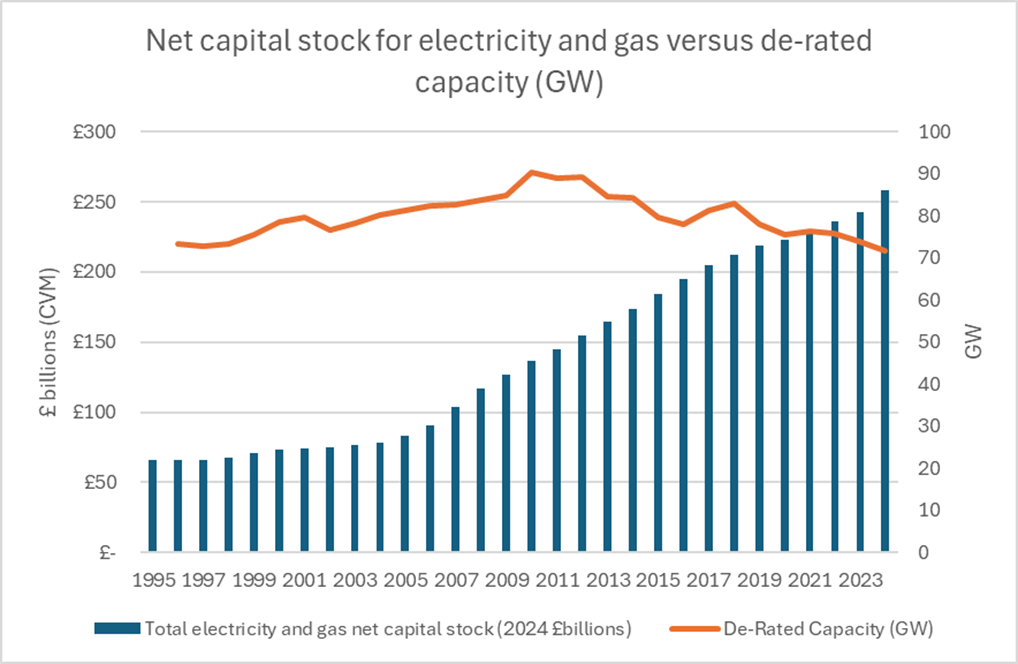

When factoring in why prices are so high, this data highlights clearly the scale of the investment that has to be paid for, through higher bills and levies. The consolation might be that we would have more capacity, and therefore could spread the cost across more generation. But this has not happened either. Generation is down from 2010. The same is true of capacity. While the nameplate capacity of the grid has ballooned, the de-rated capacity, accounting for the intermittency of renewables, has fallen from 90 gigawatts in 2010 to 72 gigawatts in 2024.

This is a tragedy of the electricity commons. If you are building a grid that has low running costs but very high capital costs, you want consumption to expand so as to spread those costs. If you wanted to draw down electricity consumption, you would opt for a grid with higher fuel costs but lower upfront costs, because those fuel costs could draw down with declining demand. We have built a grid that needs more consumption to fund it, while encouraging less electricity usage.

The takeaway is that, without the full support of the government, the UK has invested enormously in a system that has less firm capacity to produce less power at higher costs. There is little indication that, in the near future, total system costs for electricity will go down. In fact, they are expected to rise further to account for yet more transmission infrastructure.

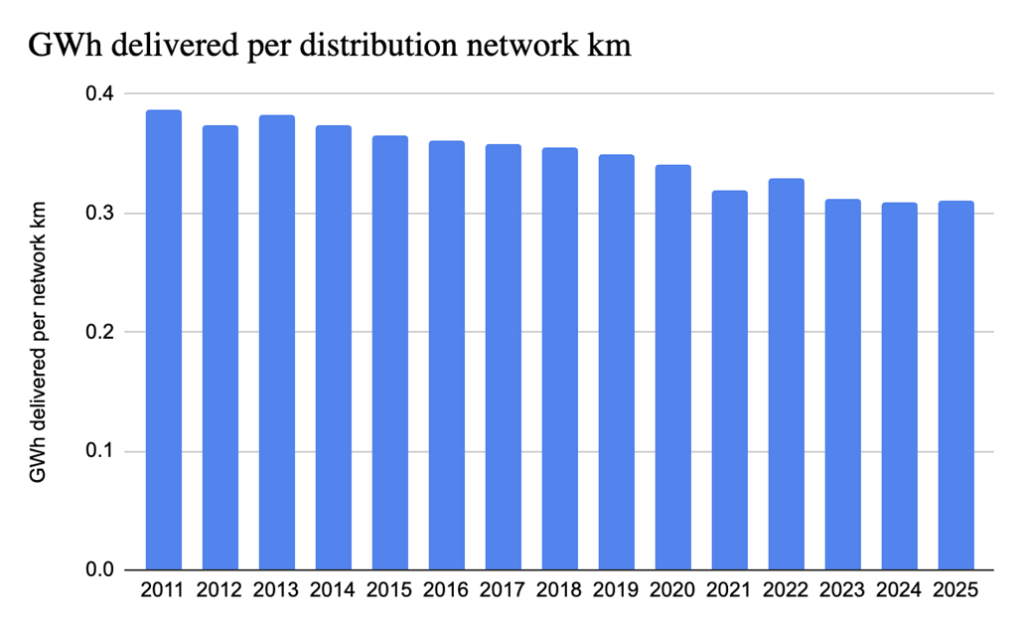

This contradiction between increased investment and infrastructure to pay for a less productive generation system can be seen everywhere. The redoubtable Ed Hezlet recently posted data from the energy regulator Ofgem. It shows that, from 2011 to 2025, network length in kilometres has grown 0.2% per year, while electricity distribution has fallen 1.3% annually, meaning electricity delivered per network-km fell by nearly 1.6% p.a. The British grid is like SpaceX’s Raptor engine development in reverse: more wires for less power.

Of course, energy investment is important and needed. But it should hopefully be a stimulant for further investment in the production sector. Instead, while electricity and gas have received unprecedented funding, the manufacturing sector, which to a large extent depends on cheap energy, has withered on the vine.

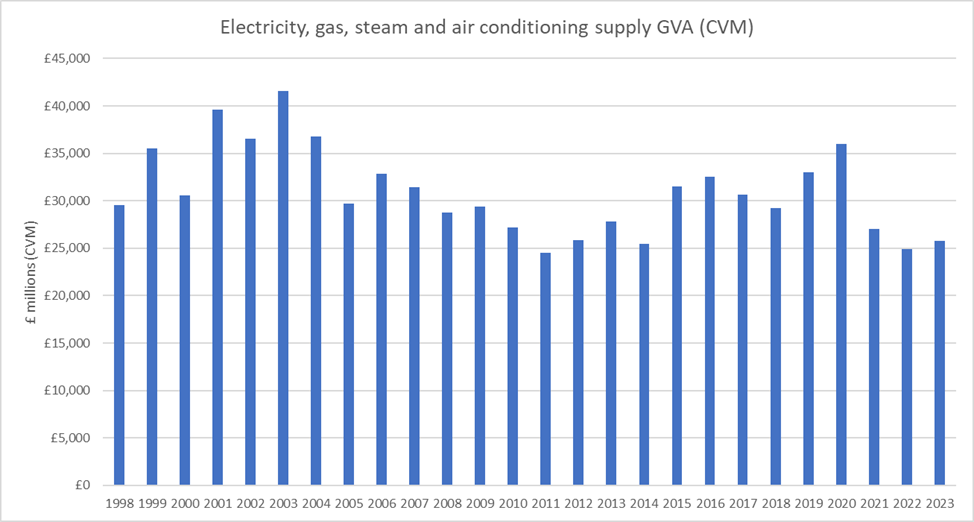

Some have argued that the green transition is good because it provides jobs and value, almost treating it the same way the Chinese might treat the car industry. But this makes no sense. The manufacturing sector has a GVA of around £200 billion. The electricity and gas sector, on the other hand, has a GVA of £26 billion as of 2023, and this has been declining over the years.

Conclusion

The energy investments could only be justified on the basis that they would make energy far cheaper, thus stimulating capital formation in industry. This has manifestly not happened and shows few signs of materialising.

Britain’s energy strategy over the last 20 years is one of the worst capital misallocations in the country’s history. The original sin was believing that a convoluted and incomplete transition to renewables and pushing electrification would do much to stimulate productivity. A renewable-heavy grid might be cleaner than a coal or gas-heavy grid, but around the world, it either costs significantly more or does not lead to significant savings. Electrification of vehicles might reduce our carbon footprint and make us less exposed to global oil shocks, but it’s not likely to bring huge productivity savings. Ditto for transitioning from gas boilers to heat pumps.

What raises productivity is success in high-value manufacturing, and on this, the British government has been completely blasé about a significant deterioration in the capital stock. The myopic obsession with Net Zero has not just distorted government attention, but seen tens of billions of pounds of private investment being misallocated in energy when it would have been better spent on those consuming the energy.

Unfortunately, given the poor situation British electricity and gas infrastructure finds itself in, there will have to be more investment going forward. A great deal of network investment is baked in, more gas plants are going to have to be built, and most parties anticipate the need to build more nuclear plants.

But if we are going to invest, we need to be laser-focused on making electricity as cheap and abundant as possible, so that we might stimulate investment in those sectors most likely to increase productivity and spur economic growth.

About the Author

Rian Chad Whitton works as a researcher for Bismarck Analysis. His Substack page, ’Doctor Syn’, is for his personal projects, focusing on automation, industrial policy, energy markets, geopolitical strategy, Britain’s place in the world and perhaps occasionally some cultural commentary. He openly states that he is not an expert: “You have been warned,” he says.

The Expose Urgently Needs Your Help…

Can you please help to keep the lights on with The Expose’s honest, reliable, powerful and truthful journalism?

Your Government & Big Tech organisations

try to silence & shut down The Expose.

So we need your help to ensure

we can continue to bring you the

facts the mainstream refuses to.

The government does not fund us

to publish lies and propaganda on their

behalf like the Mainstream Media.

Instead, we rely solely on your support. So

please support us in our efforts to bring

you honest, reliable, investigative journalism

today. It’s secure, quick and easy.

Please choose your preferred method below to show your support.

Categories: Breaking News, UK News

The infrastructure is incomplete and limits the transmission of power to points of requirement.

https://www.youtube-nocookie.com/embed/urdsJkAwWEA Bill Cooper 1993

https://www.youtube-nocookie.com/embed/YVRu6B2xt2Q John Lear interview

the Lear interview waiting approval will blow your mind

project blue book

snowbird , Aquarius , sigma

Hi Rhoda,

Just as a guide, last year I was a passenger on a 50 mile journey in UK.

I decided to count all the windmills that were turning, on the route.

On the outgoing trip, I counted 4 out of 100 that were generating,4%.

The return journey was better, there were 8 generating power, 8%.

The cost of these machines made in China, and transported to UK, and erected, would have been a fortune.

So we have a country dependent on wind, what a laugh.